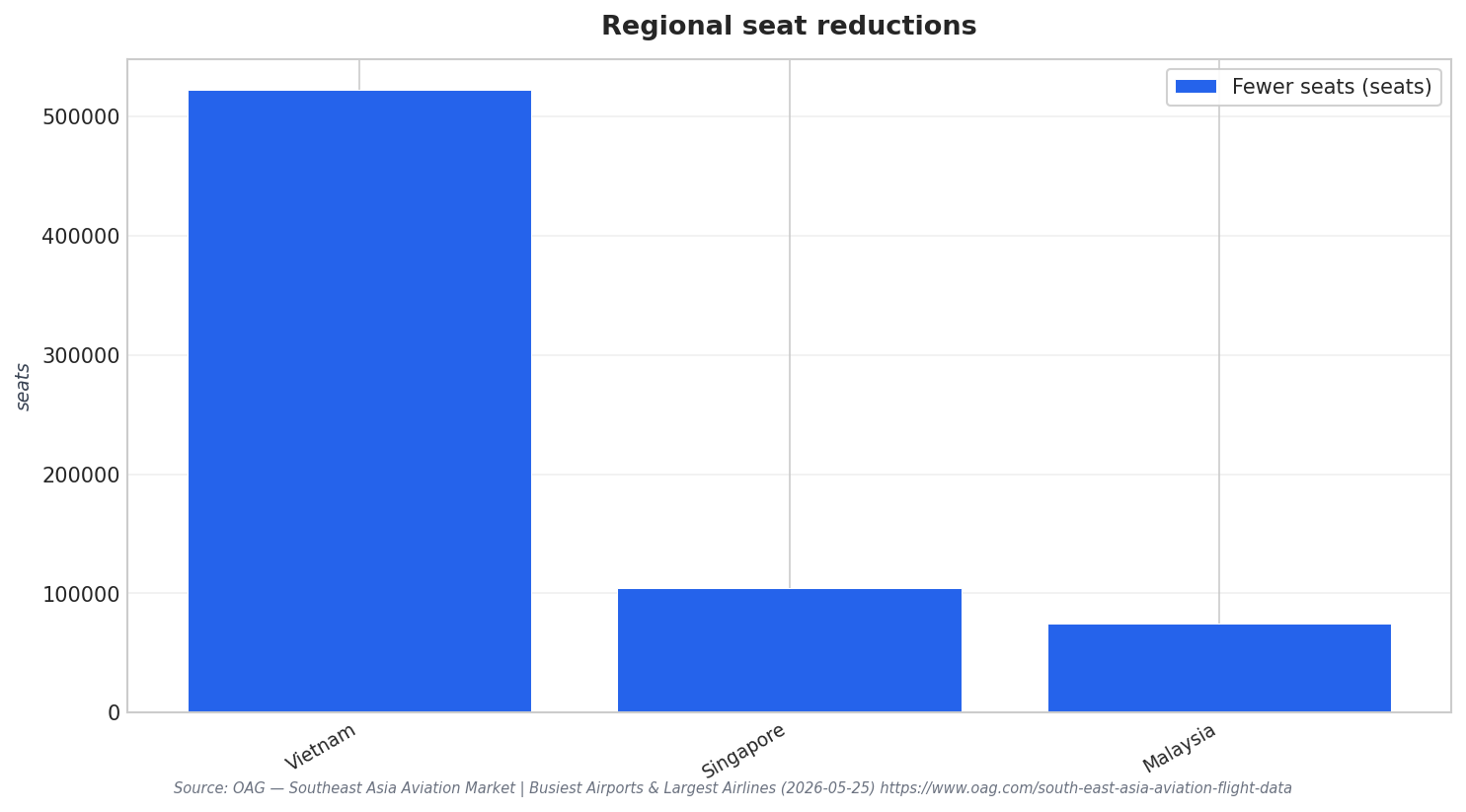

Malaysia’s aviation sector in 2026 is being pulled in two directions at once. On one hand, schedule data for Southeast Asia shows capacity has not moved in a straight line. OAG reported that capacity was reduced in Malaysia by 74,600 seats, alongside reductions in Vietnam and Singapore, in its monthly snapshot of the region. On the other hand, airline and airport strategies are signaling confidence in demand recovery, with more flights, more frequencies, and targeted route builds that aim to convert tourism momentum into sustained load factors.

Tourism is a central part of the demand narrative. Travel And Tour World reported that Malaysia recorded over 10.6 million visitors in the first quarter of 2026 alone, framing a strong backdrop for airlines adding service. The same report describes Malaysia Airlines increasing flight frequencies to markets across ASEAN, South Asia, Australia, and New Zealand to capture leisure and business traffic. It also highlights key origin markets including Singapore, China, Indonesia, India, and Australia as part of the visitor surge context, while pointing to the value of reliable connectivity as global aviation faces jet fuel price volatility and geopolitical tensions.

Routes and LCC Seat Additions: Where Growth Is Being Placed

Route-level capacity planning also shows how airlines are positioning for price-sensitive demand. In its Air Traffic Outlook 2026, the Civil Aviation Authority of Malaysia (CAAM) notes that its table of international carriers with the largest seat additions in 2026 consists entirely of low-cost carriers. CAAM interprets this as a strategic focus on price-sensitive markets and potential efforts to stimulate demand through lower fares and higher seat volumes. The same outlook links broader passenger flight increases and more wide-body services to added belly-hold capacity, supporting a more positive air cargo outlook for 2026 as passenger networks expand.

AirAsia’s own targets underline how competitive the domestic and short-haul landscape could become. Aeronewsjournal reported AirAsia’s ambition to reach 45% of the overall Malaysian aviation market and 70% of the domestic sector within the next two years, building from stated positions of 41% total market share and 60% domestic share. The same report also cites a 53% share based on 2023 figures and describes planned frequency ramps on domestic routes such as Kuala Lumpur to Penang, Kota Kinabalu, and Langkawi. AirAsia also highlighted the resumption of direct flights from Kuala Lumpur to Cebu, reflecting a route-by-route approach to rebuilding international reach.

Airport infrastructure and traveler experience are being positioned as part of the tourism tailwind as well. Travel And Tour World reported that Kuala Lumpur International Airport’s Terminal 2 ranked among the world’s best low-cost airline terminals at the 2026 Skytrax World Airport Awards. The report frames Kuala Lumpur as a leading aviation and tourism hub in Southeast Asia and ties the rise of low-cost travel to growing regional demand across Asia-Pacific markets. Put together, this is the practical Malaysia Aviation Industry Outlook for 2026: capacity may fluctuate month to month, but route additions, frequency growth, and tourism demand are pushing airlines and airports to keep building for the next wave.

What is driving Malaysia’s aviation rebound in 2026?

What does CAAM say about which airlines are adding the most seats in 2026?

How is capacity trending in Malaysia in OAG’s latest Southeast Asia snapshot?

What market share goals has AirAsia set for Malaysia?

What does the Malaysia aviation industry outlook suggest about airports and low-cost travel?