For the Malaysia foreign direct investment 2026 story, the clearest signal is the stock measure. DOSM reported that Malaysia’s FDI position increased by RM25.9 billion to RM1,113.8 billion as at the end of the first quarter of 2026, up from RM1,087.9 billion in Q4 2025. That quarter-on-quarter rise frames the question of “where it is flowing” in two ways: which economies hold the largest FDI positions in Malaysia, and what the investment pipeline implies for where future commitments may land. The same Q1 2026 release also placed the FDI movement alongside Malaysia’s wider international investment position context, including total financial assets of RM2.59 trillion and total liabilities of RM2.66 trillion.

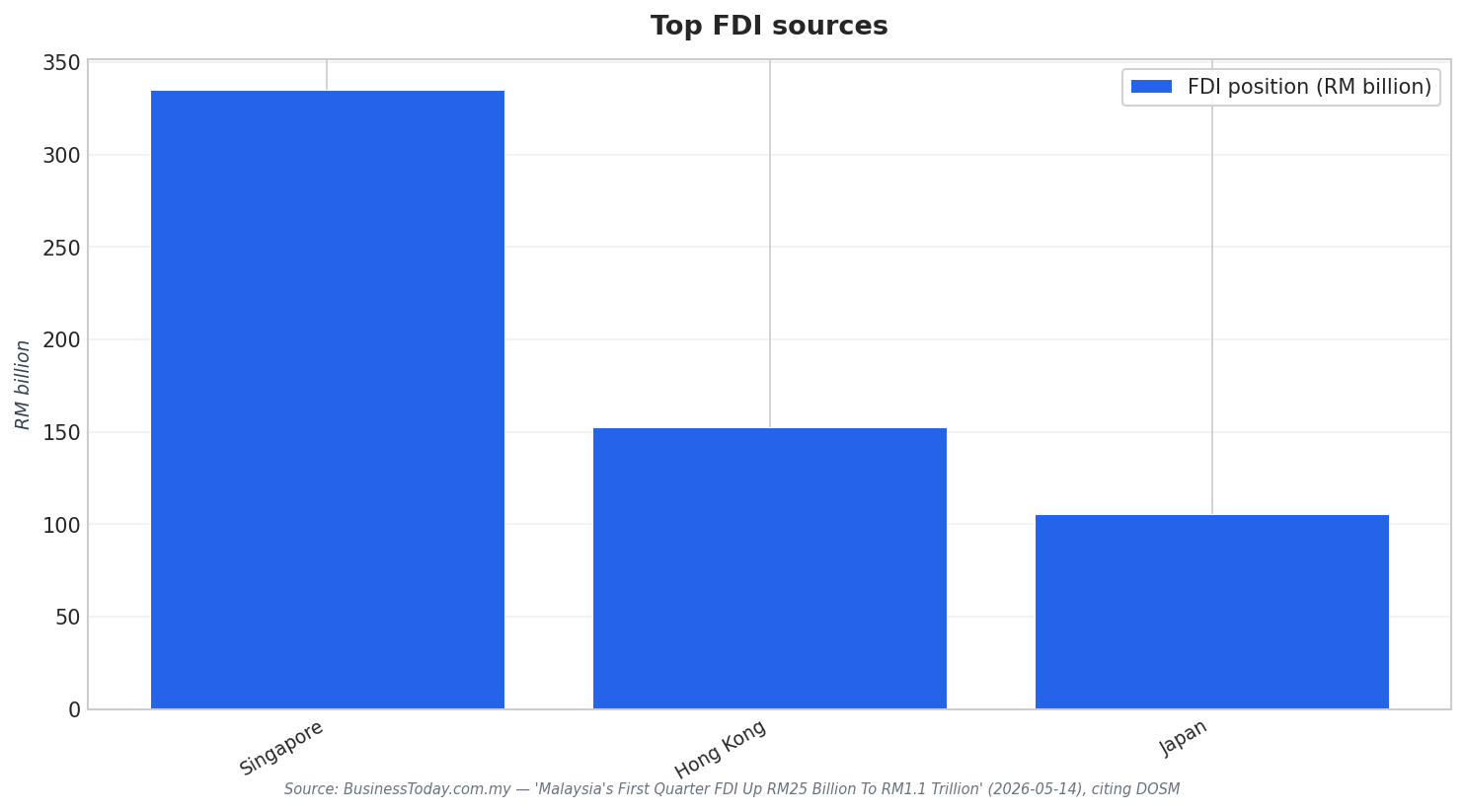

The biggest geographic sources are explicit in the Q1 2026 breakdown. The top three countries for FDI position in Malaysia were Singapore at RM335.0 billion (30.1%), Hong Kong at RM152.5 billion (13.7%), and Japan at RM105.3 billion (9.5%). Taken together, these three economies anchor the largest shares of the accumulated FDI position reported in the quarter. This helps explain why shifts in regional capital allocation and corporate expansion decisions in these hubs matter for Malaysia’s next moves. It also means that any discussion of “record” momentum in 2026 should start by tracking how these leading source countries maintain, grow, or reallocate their long-term stakes in Malaysia.

Momentum Into 2026: From the RM1 Trillion Milestone to Q1 Gains

Several releases point to a run-up into 2026 that set the stage for the Q1 increase. Acclime, citing Statistics Department data, said Malaysia’s FDI position grew from RM999.7 billion in the first half of 2025 to RM1.0215 trillion by the end of the third quarter, and noted the milestone of surpassing RM1 trillion. The same article highlighted approved investments of RM285.2 billion for the first nine months of 2025, a 13.2% increase compared to the same period in the previous year. These figures are not the same as the FDI position, but they show the scale of capital commitments and the direction of travel heading into 2026, before DOSM later recorded RM1,113.8 billion as at end-Q1 2026.

What looks like “flow” in 2026 is also reflected in what is being prepared and monitored for execution. MIDA reported that as of 2 February 2026 it was overseeing 172 pipeline projects with proposed investments totalling RM29.1 billion. MIDA also described a phased rollout that “begins with the manufacturing sector,” with a rollout to the services sector scheduled for the second quarter of 2026. This pipeline context does not replace official balance-of-payments FDI flow tables, but it does indicate where attention is concentrated and how near-term activity may be sequenced across sectors as the year progresses.

Finally, Malaysia’s 2026 FDI narrative sits in a global backdrop that is not uniformly supportive of productive investment. MIDA cited UNCTAD’s Global Investment Trends Monitor (January 2026) noting global FDI flows rose 14% in 2025, while also observing that much of the growth was concentrated in financial centres rather than productive assets, with actual investment activity subdued. Against that context, Malaysia’s Q1 2026 increase in the FDI position and the visibility of top source countries provide a grounded way to track where long-term investor interest is concentrated. For practical monitoring, DOSM’s OpenDOSM/data.gov.my catalogue publishes Malaysia’s FDI inflows, outflows, and net flows as part of balance-of-payments statistics, and notes that values for the most recent eight quarters may be revised in future releases.

What was Malaysia’s FDI position by the end of Q1 2026?

Which countries held the largest FDI positions in Malaysia in Q1 2026?

How did Malaysia’s FDI position move before 2026?

What does MIDA’s early-2026 pipeline suggest about where activity may concentrate?

What should readers track for the Malaysia foreign direct investment 2026 trend over the year?